How to do SWIFT Transfer: A Step-by-Guide

Learn how SWIFT transfers work, their benefits, and how they simplify international payments for individuals and businesses.

SWIFT transfers are a way to send and receive money internationally using a secure messaging system between banks. SWIFT is a vast messaging network used by financial institutions to quickly, accurately, and securely send and receive information, such as money transfer instructions. In this article, we explore what SWIFT does, how it works, and how to use it.

What is SWIFT?

SWIFT stands for Society for Worldwide Interbank Financial Telecommunication. It's a network that allows banks and financial institutions to securely exchange financial information and payment orders.

SWIFT transfers can be used to send money in different currencies to over 200 countries and territories.

SWIFT provides the main messaging network through which international payments are initiated. It also sells software and services to financial institutions, mostly for use on its proprietary "SWIFTNet," and assigns ISO 9362 Business Identifier Codes (BICs), popularly known as "Swift codes," and usually contain 8-11 characters.

How does Swift work?

Swift works through a combination of codes and messaging protocols. Let's take a look at the main components that go into making Swift work.

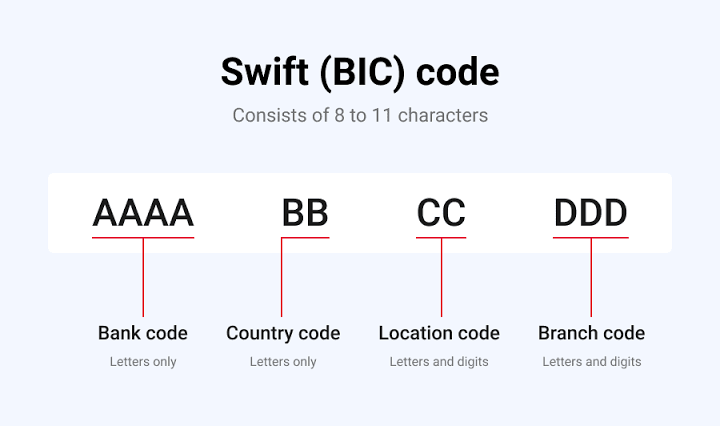

BICs

Swift assigns each financial organization a unique code, called the “‘bank identifier code”’ or BIC. It is also known as the Swift code, Swift ID, or ISO 9362 code. BIC codes are either 8 or 11 alphanumeric characters. They are made up of:

- First four characters: The institute code

- Next two characters: The country code

- Next two characters: The location/city code

- Last three characters: The organization’s branch code (optional)

Here are five examples of BICs:

- Access Bank - ABNGNGLA

- First Bank of Nigeria - FBNINGLA

- Barclays Bank (UK) - BARCGB22

- JPMorgan Chase (USA) - CHASUS33

- Bank of America (USA) - BOFAUS3N

Behind each BIC, SWIFT stores information about the institution, such as its legal name, registered address, and business type. Members must confirm these details at least once per year or whenever there is a change.

SwiftNet

Swift’s messaging platform is called SwiftNet. It uses hundreds of different codes to distinguish between different types of cross-border payments and money transfers. These are grouped into 10 categories:

- Category 1: Customer Payments and Cheques

- Category 2: Financial Institution Transfers

- Category 3: Treasury Markets: Foreign Exchange, Money Markets, and Derivatives

- Category 4: Collections and Cash Letters

- Category 5: Securities Markets

- Category 6: Reference Data

- Category 6: Treasury Markets: Commodities

- Category 7: Documentary Credits and Guarantees/Standby Letters of Credit

- Category 8: Travelers Cheques

- Category 9: Cash Management and Customer Status

- Category 10: Common Group Messages

Here's how a SWIFT transfer works:

- Initiate the transfer: A client requests a SWIFT payment from their bank.

- Send the message: The client's bank sends a secure message through the SWIFT network to the recipient's bank. The message includes the recipient's account details and the amount to be transferred.

- Receive and process the message: The recipient's bank receives the message and processes it. e

- Credit the funds: The recipient's bank credits the funds to the intended account.

- Notify the client: The SWIFT system changes the payment status, and the client is notified of the result.

Note: Timeframes for SWIFT transfers (typically 1-5 business days)

Costs and fees associated with SWIFT transfers

SWIFT transfers can incur several fees, including:

- Outgoing wire transfer fee

- Charged by the sender's bank, this fee varies by the amount and destination.

- Incoming payment fee

- Charged by the recipient's bank for processing the transfer

- Foreign exchange fee

- Charged when converting funds into another currency. This fee can vary depending on the exchange rate and the bank's policy.

SWIFT tracing fee

This is charged if a transaction is delayed or if there is a problem with the payment.

Correspondent fee

A correspondent fee is charged by banks in the SWIFT network, which helps facilitate the transfer of money from one country to another. Banks usually pass on the fees they pay to SWIFT to their clients through per-transaction fees. The amount that other banks can charge you can vary, but estimates suggest anywhere between €15 and $50 or equivalent.

Benefits of SWIFT Transfers

- Security: SWIFT's encrypted messaging platform protects sensitive financial information during transfers.

- Global reach: SWIFT covers more than 200 countries, allowing financial transactions to take place almost anywhere in the world.

- Data protection: SWIFT's secure financial messaging services encrypt and protect the data being transferred.

- Versatility: SWIFT transactions can be made in all major currencies.

- Speed: SWIFT financial transactions are executed within 1-3 business days.

- Cost-efficiency: SWIFT reduces the cost of cross-border payments and money transfers.

- Tracking: SWIFT transfers are traceable along the network, so you can check the status of a transfer if it's taking longer than expected.

- Connectivity: SWIFT offers a highly reliable, secure, and robust connection.

- Payment controls: SWIFT's Payment controls feature uses unique data from the entire SWIFT network to detect anomalies at the account level.

How to Make a SWIFT Transaction

To make a SWIFT transaction, follow these steps:

- Contact your bank: Provide them with the details of the transaction. This includes the recipient’s name, bank name, account number, amount, currency, and any other relevant information.

- Complete the required forms: Your bank will provide you with the necessary forms to initiate the SWIFT transaction. These forms will typically include information on the originator and beneficiary of the transaction, the amount to be transferred, and the currency involved.

- Provide payment: Once the forms are completed, you will need to provide payment. This typically involves transferring the funds from your account to your bank’s account.

- Wait for confirmation: Once the transaction has been initiated, you will need to wait for confirmation that the funds have been transferred successfully. This can take several hours or even days, depending on the banks involved and the complexity of the transaction.

SWIFT transactions can be costly, especially for smaller transactions, as they often involve fees and charges from multiple banks involved. You should also ensure that you provide accurate and complete information to avoid delays or errors in processing.

Safety and security involved in SWIFT transfers

Encryption SWIFT encrypts payment instructions and data flows to protect against fraud and unauthorized access.

Authentication SWIFT uses authentication and digital signatures to ensure that only authorized parties can access the network.

Regulatory compliance

SWIFT requires participating banks to adhere to security and operational standards, as well as international anti-money laundering (AML) and Know Your Customer (KYC) regulations.

Security audits SWIFT audits its security measures to ensure they are effective.

Customer verification both the sending and receiving banks verify account numbers, routing numbers, and the identities of the parties involved.

IBAN

The International Bank Account Number (IBAN) reduces errors by providing an additional verification level for account details.

While SWIFT transfers are a secure and efficient way to send money internationally through a trusted global network, understanding how it works can help you manage international transfer.

Discussion